(PA) 610-572-2034

(DE) 302-358-2114

Family Education

A Service Brought To You By Four Seasons Healthcare

A Service Brought To You By Four Seasons Healthcare

![]()

Medicaid

Medicaid will pay for long term care in some circumstances.

To qualify for Medicaid an individual must have limited income and few assets. If care must be provided in a nursing home, you probably won’t have a choice of which nursing home.

Medicaid is a joint State/Federal medical insurance program for the “poor” and indigent. Unlike Medicare, it pays for both skilled and custodial care. Eligibility rules are complicated and vary from state to state, but in general the recipient must have no more than $2,000 in personal assets (the home up to $500,000 is exempt, as is 1 car, jewelry and some other possessions), and can keep only about $30/month in income for personal needs. Everything else goes to the state to pay for the care provided, including any pension and/or Social Security income.

The spouse of someone on Medicaid may stay in the family home and keep some assets (~$80,000) and income (~$2000/month). Amounts vary from state to state.

One of the disadvantages of relying on Medicaid is that you will be limited to which facility you can go to. There are only a limited number of Medicaid beds available in a nursing home, provided they take Medicaid at all. We don’t like to make sweeping generalizations, but the reality tends to be that Medicaid pays about half of the “market rate” for nursing care. As a result, there is a tendency for these facilities to have overworked and underpaid staff.

See Waiver Programs for an alternative to Medicaid facility care.

There are ways to structure your estate with such vehicles as trusts and annuities, or the conversion of Medicaid countable assets to non-countable assets that will enable you to legally qualify for Medicaid without “spending down” all of your assets. It’s important that you seek advice on your particular situation from an experienced and certified Elder Law Attorney. Don’t just try to “hide” assets or forget about “gifts” made to family members on your Medicaid application. Medicaid has a “look back period” of 5 years from the date of application during which any gifts made by the Medicaid applicant must be counted.

There are ways to structure your estate with such vehicles as trusts and annuities, or the conversion of Medicaid countable assets to non-countable assets that will enable you to legally qualify for Medicaid without “spending down” all of your assets. It’s important that you seek advice on your particular situation from an experienced and certified Elder Law Attorney. Don’t just try to “hide” assets or forget about “gifts” made to family members on your Medicaid application. Medicaid has a “look back period” of 5 years from the date of application during which any gifts made by the Medicaid applicant must be counted.

Medicaid Waivers

![]()

At one time, Medicaid dollars only paid for institutional services. Today, Medicaid allows states to define and provide more diverse services and supports for individuals in the community, by "waiving" the need to get those same services in an institution.

At one time, Medicaid dollars only paid for institutional services. Today, Medicaid allows states to define and provide more diverse services and supports for individuals in the community, by "waiving" the need to get those same services in an institution.

Delaware

What services are available in Delaware for long-term care coverage?

If an individual who is a resident of Delaware meets the medical and Medicaid financial eligibility requirements, the Delaware Division of Social Services can pay for long-term care through three Medicaid programs:

1. Nursing Facility program

2. Long Term Acute Care program

3. Waivers

- HCBS Waiver (Home & Community Based Services)

- Elderly and Disabled Waiver,

- AIDS Waiver,

- Mental Retardation Waiver,

- Assisted Living Waiver.

How do I begin the process for Medicaid payment for long-term care services?

First, a referral must be made (usually by phone). For:

- Nursing home care call the Pre-Admission Screening (PAS) unit.

- Elderly and Disabled Waiver services call the Division of Services for Aging and Adults with Physical Disabilities (DSAAPD) .

Upon referral, arrangements will be made for a medical team, consisting of a nurse and a social worker case manager from the PAS unit, to visit the applicant and evaluate him/her medically to determine if he/she requires a skilled or intermediate level of care (LOC) as defined by Delaware Medicaid criteria.

If the applicant is found medically to have a need for skilled or intermediate level of care, the PAS unit will refer the applicant to the Financial Eligibility unit which will determine his/her financial eligibility for Long-term Care services.

If the PAS team does not leave an application packet, the financial unit will send the packet to the applicant or family contact. The person receiving the packet is instructed to call the office for an appointment with a social worker case manager.

The applicant or family contact should complete the application prior to the interview but not sign the application. All information relating to the application should be brought to the interview so that an accurate and timely determination of eligibility can be made. If the social worker case managers needs further documentation, a letter will be given to the applicant or family member stating what items are still needed.

Once all of the information has been received, and if the applicant is determined to be eligible financially, Medicaid may begin payments for long-term care services at the time of institutionalization. "Institutionalization" would be placement in a nursing facility or receipt of community based services in the home.

** Note: Applicants must be medically in need of a skilled or intermediate level of care as defined by Delaware Medicaid criteria and must be financially eligible to qualify for either the nursing home or community based long-term care services.

See the Medicaid section of Long Term Care Funding.

Pennsylvania has six waiver programs:

Aging Waiver (PDA Waiver) – provides long-term care services to qualified older Pennsylvanians living in their homes and communities. Following is a list of services available through the Aging Waiver that may be available to you:

- Adult Daily Living Services

- Community Transition Services

- Companion Services

- Counseling Services

- Environmental Modifications

- Financial Management Services

- Home Delivered Meals

- Home Health Services

- Home Support Services

- Non-Medical Transportation Services

- Participant-Directed Goods and Services

- Participant-Directed Community Supports

- Personal Assistance Services

- Personal Care Services

- Personal Emergency Response System

- Respite Services

- Specialized Medical Equipment and Supplies

- TeleCare

There is no cap on the services that Aging Waiver participants receive, no cost sharing and no contributions allowed. In order to qualify for Aging Waiver services, you must meet eligibility requirements. This includes a level of care assessment and a determination of financial eligibility. (For Chester County, PA 2009: Individual Income at or below $2,022 per month and Individual Assets at or below $8,000.)

For more information, contact your local area Agency on Aging.

AIDS Waiver – provides home and community based services to eligible persons age 21 or older or who have symptomatic HIV Disease or AIDS.

Attendant Care Waiver/Act 150 Program – Information for mentally-alert Pennsylvanians with physical disabilities.

COMMCARE Waiver – Home and community-based program developed for individuals who experience a medically determinable diagnosis of traumatic  brain injury.

brain injury.

Independence Waiver – provides services to persons with physical disabilities to allow them to live in the community and remain as independent as possible.

OBRA Waiver – provides services to persons with severe developmental physical disabilities, such as cerebral palsy, epilepsy or similar conditions.

Medicare/Medicare Supplemental Insurance

In most cases Medicare will not pay for long term care.

Most people are surprised to find out that, unfortunately, Medicare does not pay for long term care and it was never intended to.

The only government programs that cover an individual needing help with Activities of Daily Living are Medicaid and the Veterans Administration.

Medicare was intended to cover acute skilled care (usually after a hospital stay), but chronic care such as the need for ongoing help with ADLs (eg frailty due to aging or a progressive disease) is not covered by Medicare or Medicare Supplemental policies.

This rule applies to long term chronic care in any setting, including a nursing home. If a Medicare recipient requires a hospital stay of 3 days and 3 nights, Medicare will cover a portion of the cost of care in a nursing home (skilled facility) for up to 100 days.

This rule applies to long term chronic care in any setting, including a nursing home. If a Medicare recipient requires a hospital stay of 3 days and 3 nights, Medicare will cover a portion of the cost of care in a nursing home (skilled facility) for up to 100 days.

If the care you are receiving is considered custodial (and 85% of nursing home care is) rather than skilled medical care, then your stay is not covered. No matter what, after 100 days, Medicare stops paying and it’s up to you. In other words, Medicare covers a hospital stay that results from a fall but it does not cover the help that would have prevented a fall.

Viatical Settlements

A viatical settlement is the sale of an existing life insurance policy to a third party for more than its cash value but less than its death benefit.

Proceeds from viatical settlements can be used for any purpose, including financing senior living and home care needs. Viatical settlements are only possible if you are terminally ill, which in this case generally means that you have a life expectancy of two years or less.

A Viatical Company pays you an amount of money based on a percentage of the death benefit of your life insurance policy. The amount you receive is based upon your life expectancy.

The Viatical Company then owns the policy and is its beneficiary, and it takes over payment of premiums on the policy. As a result, you get money to pay for care, and the Viatical Company receives the full death benefit after you die.

Unlike a Life Settlement, money you receive from a Viatical Settlement is tax-free, provided you have a life expectancy of two years or less, or are chronically ill.

The Viatical Company must be licensed in the states in which it does business.

Private Funds

Most people currently pay for home care, assisted living and retirement communities out of their own pockets with private funds. Private funds account for 90% of assisted living payments.

About one third of long term care at nursing facilities is funded with private funds.

Early planning with Long Term Care insurance or estate structuring with the help of an elder law attorney can offset the potentially devastating costs of long term care.

Long Term Care Insurance

Long term care insurance helps cover the cost of care at home or in a nursing facility while protecting your assets. Long Term Care policies are sold by private insurance companies or agents, and are increasingly being offered as benefits by employers.

If you are over 50 and expect to retire with more than $70,000 in assets, you should consider buying Long Term Care insurance. Current nursing home rates in PA are $84,000 per year and $87,840 in DE. Average nursing home stays are 2.6 years which equals upwards of $218,000. Projected costs in 2030 are $190,000 per year, or $495,000.

The odds of needing Long Term Care are high. The probability of becoming disabled in at least two activities of daily living or of being cognitively impaired is 68% for people age 65 and older. While Americans are living longer, they're not necessarily living healthier. The prevalence of cognitive impairment among the elderly has increased dramatically over the past decade, while the prevalence of physical impairment remains unchanged.

Currently, 22% of people over age 85 are in a nursing home and about half of those over age 85 who are not in a care facility require some assistance. But early planning can help offset the potentially devastating costs of Long Term Care.

The average buyer of individual Long Term Care insurance in America is approximately 58 years of age depending on the study you read. This statistic has decreased dramatically from the high 70s only a decade ago. In employer-sponsored plans, the average age LTCi buyer is only 41.

The Federal Government has also offered LTCi coverage to all federal employees, spouses and dependents - 20 million Americans! However, they have not subsidized the cost. This makes a significant statement to the baby boomers of this country. Go out and buy LTC insurance! Every year that a person waits to buy Long Term Care insurance could cost them 10% to 12% in premiums.

When should you buy Long Term Care insurance?

Premiums are based on age. For those of you who purchase inflation protection (and this should be all of you) the cumulative costs of the premiums is going to be lower the earlier you buy. You do not "save" premiums by waiting. Because Long Term Care Insurance premiums rise substantially with age, the earlier you buy LTC insurance the lower your cumulative insurance premiums will be.

You never save money by waiting, but you do lose benefits.

The chart below shows an example of a policy that pays $200 per day for 4 years and includes compound inflation protection.

The above example assumes that the individual applying for coverage has the same health history at age 75 as at age 55. In reality, most people's health declines with age which adversely affects premiums and even the ability to obtain insurance. If you have assets to protect and can afford the premium without changing your lifestyle, now is the best age to buy Long Term Care Insurance.

Good Health Discounts -- Your health history can also affect premiums by as much as 150%. So if you are in good health, it can pay to purchase early to lock in advantageous rates. On the other hand, if you have a serious medical condition, you may be unable to find coverage at any price.

Spousal Discounts -- Married people can get discounts of 10 to 35% annually. For many couples these discounts will also apply to committed couples that are cohabiting. These discounts can even apply to brother & sisters.

Tax Deductions -- LTC insurance premiums on tax-qualified policies are considered medical expenses under current IRS guidelines. If your total medical expenses exceed 7.5% of your adjusted gross income, you can write off the excess as an itemized deduction on Schedule A.

Even Better Tax Deductions -- If you're a sole proprietor, partner or LLC owner, you can deduct all of the premiums for a qualified long-term-care policy whether or not you itemize.

Group Discounts -- If you work for a company that offers Long Term Care insurance, you may be able to get lower priced group coverage. Although be aware that many of these group policies have significantly reduced benefits or non-standard qualification criteria. Better yet, if you are an executive or owner of a business it is possible to provide Long Term Care insurance to a subset of employees. These "executive carve-out" policies are exactly the same as standard individual policies but with 10-15% premium discounts and often with significantly lower underwriting requirements.

Plan Design - Smaller Policy -- By opting to co-insure part of the cost of care you can significantly reduce your premiums. For instance, lowering your daily benefit by 20% will provide you with a 20% lower premium. Opting for a 4 year policy rather than 6 year can reduce costs 15-30% annually.

Plan Design - Longer Elimination Period -- The elimination period is essentially a deductible for Long Term Care insurance. It is the amount of time that you pay out of pocket (or from an alternative source like Medicare or your health insurance) before the policy starts to pay. Increasing your elimination period from 0 to 90 days can save you 10 to 15% annually.

Annual Premium Payments -- You can save 8% a year just by sending your payment in one lump sum on your anniversary date. Don't worry, this is an anniversary you won't forget as the carrier will kindly send you a premium notice. An insurance agent can help you find a policy that's both affordable and represents the best value for someone of your age and situation.

Partnership-Certified Plans -- A Long-Term Care insurance policy approved by your state for participation in the partnership program. This program allows you to receive benefits from Medicaid for Long Term Care services without spending-down all of your assets if you have previously purchased and depleted the benefits in a partnership-certified policy. This program is not currently available in every state but it is available in Pennsylvania and Delaware. Be sure to seek a LTC insurance policy that is partnership-certified! The premium is the same, the underwriting is the same, and the benefit structure is the same. What makes a partnership-certified policy different is the State’s match (dollar for dollar) of Medicaid spend-down requirements. If the need arises, it allows policyholders to go on Medicaid with a higher level of assets and/or income than would otherwise be allowed.

Case Study:

The following is an example of how a Partnership qualified policy works. Let's say John, a single man, purchases a Partnership policy with a value of $100,000. Some years later, he receives benefits up to the policy's lifetime maximum coverage (adjusted for inflation) equaling $150,000. John eventually requires more long term care services and applies for Medicaid. If John's policy was not a Partnership policy, he would be entitled to keep only $2,000 in assets in order to be eligible for Medicaid. He would have to spend down any assets over and above this amount. However, because John bought a Partnership policy, he can keep $152,000 in assets and the state will not recover those funds after his death. However, any assets John has over and above the $152,000 would have to be spent in order for him to be eligible for Medicaid. He would also have to satisfy the income, general eligibility and functional eligibility requirements for Medicaid before he can qualify.

Is it hard to qualify for LTCi?

Over 75% of all applicants are being approved for coverage. It is much harder to qualify for a disability, health or life insurance policy medically. Many people who apply for LTCi are taking multiple medications, could possibly have had a history of cancer, heart problems or even diabetes. The key is control. Companies want to see that you are stable and that you don't have conditions that will cause you to become disabled. You will even be eligible for preferred health discounts if you are squeaky clean.

However, Long Term Care insurance is not right for everybody. Whether or not you should purchase a policy depends on your health, income and assets. If you are retired, with less than $70,000 in assets (not including your home and car) or your only income is your Social Security or SSI benefits, you probably shouldn't be purchasing Long Term Care insurance. There are no hard and fast rules however. $70,000 in Omaha is not the same as $70,000 in Manhattan and everyone's family and health situation is different. Nevertheless, the premiums should be affordable, even if they increased by 25%, without significantly changing your lifestyle. Nobody should have to eat tuna fish every night in order to pay for Long Term Care insurance premiums!

Reverse Mortgages

A reverse mortgage is a loan against the equity in your home that you do not have to pay back as long as you live there.

You can turn home equity into cash that you can use for your home care.

You will not need to move or make monthly payments. The most common type of reverse mortgage is the Home Equity Conversion Mortgage (HECM) which completely protects your ability to remain in your home.

So long as you pay your property taxes and homeowners insurance and maintain your property, you can remain in your home forever.

If the reverse mortgage lender fails, any unmet payment obligation to the borrower will be assumed by FHA. In 2009 about 130,000 HECMs were written, and feedback from borrowers has been mostly positive. In a recent survey of borrowers by AARP, 93% said that their reverse mortgage had a mostly positive effect on their lives.

For many, a reverse mortgage is the best way, and often the only way, for them to be able to afford to remain at home.

You should however, investigate eligibility for the VA or Medicaid benefits first.

Veterans Administration

If you are a United States veteran or surviving spouse of a veteran, you may qualify for the Aid & Attendance Program and receive monthly benefits to help cover the costs of your home care. The Department of Veteran Affairs (VA) considers the Aid and Attendance program as one of their most underutilized offerings.

Here's why: most veterans do not know about it, or how to apply.

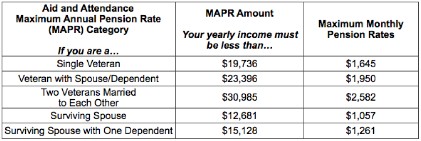

This is a "pension benefit" and is not dependent upon service-related injuries for compensation. This Special Pension which is part of the VA Improved Pension program, allows for Veterans and surviving spouses who require the regular attendance of another person to assist in eating, bathing, dressing, etc to receive additional monetary benefits. It also includes individuals who are blind or a patient in a nursing home because of mental or physical incapacity. Assisted care in an assisted living facility also qualifies. Most Veterans who are in need of assistance qualify for this tax free pension.

To qualify you must meet the following guidelines. Note that these are guidelines, not hard and fast rules. Also note that there are means of planning ahead to legally meet the asset guidelines.

The veteran must have served at least 1 day during war time and 90 consecutive days active duty.

Had an honorable or general discharge.

A widowed spouse applying for benefits must have been married to the Veteran at the time of the Veteran’s death and never remarried.

Total liquid assets cannot exceed $80,000 (stocks, bonds, CDs, IRA, 401k, annuities, savings, cash, etc). House, auto & personal property is exempt.

You must have a doctor’s order insisting you need the help.

Following is a table of benefits.

It will probably take 3-6 months to process your claim, but if you qualify you would receive a check for the amount accrued since the date you submitted the application.

Senior Living Line of Credit

A typically unsecured line of credit against which you can borrow only what you need.

This type of solution may give you the time you need to sell an asset such as a house, stock, or even wait for CDs that need to mature.

A Senior Living Line of Credit can give you the flexibility of waiting for improved market conditions before selling a home or stock, or give you time to remodel in order to command a higher price. It can free you from the need to accept the first lowball offer on an asset because you are strapped for cash.

You can typically get same-day decisions and quick (24-48 hour) funding, and up to six persons can usually apply together so one sibling is not carrying the whole burden.

Additional State & Local Programs

A wide variety of services is available to qualifying seniors through the local office of aging (see links). The key here is “qualifying”. These services can range from transportation, to meal delivery, to legal advice, and the Department will usually have care managers assigned to your case to help guide you through which services are available to you. There are also Home and Community Based (HCBS) “waiver” programs (see link opposite for Waiver Programs).

For those who don’t financially qualify for waiver programs, the Department of Aging usually has some sort of “cost sharing” program. In Pennsylvania, “Options Programs” will look at your individual case to determine what services they can offer. You’ll typically be awarded a certain “chunk” of money and the county Care Manager will work with you to determine how that money is spent.

Life Settlements

A life settlement gives you the ability to raise cash by selling your life insurance policy.

With a Life Settlement, you sell your life insurance policy for its present value. Life settlements are usually only available to women age 74 and older and to men age 70 and older.

The proceeds may be used for any reason, such as paying long term care insurance premiums or paying for long term care services directly. Health screenings are not usually required; you may be in good or poor health.

There may be tax liabilities on the proceeds of the sale.

All the information on this web site is published in good faith and for general information purpose only. We do not make any warranties about the completeness, reliability and accuracy of this information. Any action you take upon the information on our web site is strictly at your own risk. We will not be liable for any losses and damages in connection with the use of this web site.

From our web site, you can visit other web sites by following hyperlinks to these sites. While we strive to provide only links to useful and ethical websites, we have no control over the content and nature of these sites and the links to other web sites do not imply a recommendation for any or all the content found on these sites. Please be also aware that when you leave our web site, other sites may have different privacy policies and terms which are beyond our control.